Since 2021, the California LCFS credit market experienced a persistent surplus, with credit creation consistently surpassing compliance needs. This led to an ever-growing credit bank, plummeting prices that stayed at rock-bottom levels. Nevertheless, this trend is now shifting.

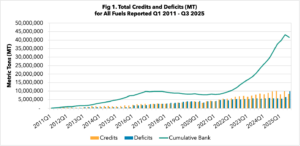

Figure 1 California Credit Bank: CARB’s published data showed the first quarterly deficit in many years. Because LCFS reporting lags by approximately seven months, Q3 represents the first observable impact of the 2025 step change –CARB

The credit bank remains substantial; what has shifted is its trajectory. This change is driven by the 9% market adjustment incorporated into the 2025 regulatory update. While one quarter alone doesn’t wipe out a large credit bank, in markets, direction is as important as size. A system that is building inventory operates very differently from one that is reducing it.

For years, the LCFS functioned as a surplus market with ample optionality. Obligated parties had the ability to postpone purchases with minimal risk. Generators operated in an oversupplied environment, competing amid a market anchored by price floors and expectations of increasing inventory.

The 2025 stringency step change has shifted the trajectory. The system has moved from a structural surplus to a structural deficit, causing prices to now reflect factors like investment ROI, bank drawdown rates, supply elasticity, and expectations of future regulatory updates. LCFS credits, which had traded near their floor for a long time due to inventory build-up reducing urgency, are now influenced by a decreasing bank, changing market psychology. Markets are beginning to price in future scarcity before the system becomes critically tight. The earlier uncertainties about the timing and location of regulatory changes have disappeared. We can now observe the initial effects.

EcoEngineers’ LCFS Credit Outlook Provides the Answers

EcoEngineers recognized the early signs of a price collapse driven by surplus, based on expanding renewable diesel capacity and bank growth patterns. Currently, the same balance-sheet analysis suggests ongoing depletion.

We have created a forward-looking model that assesses future bank depletion across various supply scenarios, adjusts for scarcity pricing behaviors, and establishes risk-adjusted price ranges linked to inventory reduction.

Our updated LCFS Credit Outlook provides:

- Scenario-based bank projections

- Risk-weighted price ranges

- Strategic considerations for obligated parties, credit generators, and investors in this evolving market phase

After years of increasing surpluses and floor-level prices, the LCFS market is beginning to reflect a different reality; instead of pricing in abundance, it is beginning to price in scarcity.

The question is no longer whether the LCFS is oversupplied. The data show the direction has shifted.

For market participants, the critical variable is not today’s bank size — it is the speed of change. In a tightening system, timing, procurement strategy, and capital allocation decisions become materially more consequential.

The surplus era created complacency. The next phase will reward foresight.

To purchase EcoEngineers’ LCFS Credit Outlook, contact us at clientservices@ecoengineers.us.

You can also join EcoEngineers at the upcoming EcoForum series, where our experts will unpack the data, explore forward scenarios, and discuss what this new CA-LCFS phase means for compliance strategy, project development, and investment decisions. Link here for more information: https://www.ecoengineers.us/ecoforums/