Understanding and Measuring the Environmental Impact of Clean Hydrogen Production with LCA

New Policies and Tax Credits Require Quantifiable Emissions

By Tanya Peacock, EcoEngineers

As the world seeks sustainable energy solutions, clean hydrogen is emerging as a promising option among various approaches to decarbonization. Its potential to revolutionize energy consumption is particularly notable in heavy industries and transportation sectors where decarbonization poses significant challenges. To better understand hydrogen’s role in the energy transition alongside other decarbonization strategies, we need to understand the environmental aspects of producing, transporting, and using clean hydrogen.

The Importance of Life-Cycle Analysis (LCA)

LCA has emerged as a key tool in understanding the environmental impacts of not only hydrogen production but also a myriad of low-carbon fuels and pathways. This methodical approach accounts for the emissions across a product’s life stages. From extraction to disposal, LCA quantifies carbon emissions across various production pathways and is essential for transitioning to cleaner energy.

Recent policies, including the Inflation Reduction Act (IRA), have made it imperative to quantify life-cycle greenhouse gas (GHG) emissions for hydrogen on a well-to-gate life-cycle basis to qualify for the new 45V clean hydrogen production tax credit. This guidance, which offers up to $3 per kilogram of hydrogen with a carbon intensity (CI) below certain thresholds, underscores the importance of LCA models like the Argonne National Laboratory’s Greenhouse Gases, Regulated Emissions, and Energy Use in Technologies (GREET) model used in government support mechanisms such as the 45V clean hydrogen production tax credit.

Making Clean Hydrogen Cleaner

The quest for cleaner hydrogen has drawn attention to blue and grey hydrogen projects, and its sustainability continues to be a point of focus. One innovative strategy for improving hydrogen’s environmental attributes involves leveraging renewable natural gas (RNG) credits. Market mechanisms like California’s Low Carbon Fuel Standard (LCFS) encourage RNG’s use for CI reduction by employing a book-and-claim system — a common accounting method where a sustainability claim made by a company is separated from the physical flow of these commodities. Yet, the proposed 45V clean hydrogen tax credit guidance from the U.S. Treasury and Internal Revenue Service (IRS), while allowing RNG use, awaits further clarification on compliance. The U.S. Department of Energy (DOE) also requires additional validation if RNG feedstock does not fit within the parameters of the 45VH2-GREET model.

Carbon capture and storage (CCS) is another critical component in the clean hydrogen narrative, and its potential to enable large-scale clean hydrogen production is significant. By utilizing established infrastructure and benefiting from economies of scale, CCS can be a powerful ally toward net-zero goals, especially with the financial incentive of 45V tax credits.

The U.S. Environmental Protection Agency (USEPA) has not yet approved any hydrogen pathways for Renewable Identification Number (RIN) generation under the Renewable Fuel Standard (RFS). Multiple pathway petitions have been filed by EcoEngineers and others on behalf of their hydrogen clients.

Clean Hydrogen Future Hinges on Low-Carbon Pathways

Hydrogen production from unconventional sources, such as dairy manure, requires detailed LCAs to calculate the CI accurately. The technology choice for hydrogen production, from steam methane reforming (SMR) to electrolysis powered by renewable energy, directly influences the CI score derived from LCA. Producers are motivated to lower their CI not just to comply with regulations but to monetize credits and/or tax incentives and to meet sustainability targets.

The 45V clean hydrogen production tax credit guidance also outlines criteria for sourcing renewable power for hydrogen production. While on-site production is an option for some projects, any grid power used must be verified as renewable through Energy Attribute Certificates (EACs), adhering to strict registration and accounting standards.

Additionally, producers of clean hydrogen face the ongoing task of updating their LCA in alignment with GREET model revisions. The IRA mandates annual LCA updates, ensuring that life-cycle GHG emissions rate calculations are based on the latest data. Additionally, the LCA must address co-products and their emissions, with a clear methodology from regulatory bodies to ensure fair assessments, especially regarding emission allocations to co-products or crediting clean hydrogen production when displacing less clean hydrogen. Also required are annual verification reports performed by an unrelated party.

Summary

Understanding the CI of hydrogen is not just about regulatory compliance; it’s a business imperative. Project developers are incentivized to explore technology options and process improvements to reduce the CI of their hydrogen. Comprehensive LCA services are invaluable, assessing hydrogen CI and identifying strategies for carbon reduction. These services support project developers and policymakers in making informed decisions that align with environmental and economic objectives, aiming to create a transparent, consistent, and fair clean hydrogen market that reflects the true environmental costs and benefits of production methods.

Integrating RNG credits, alongside strategic use of CCS and meticulous LCAs is critical for hydrogen production’s evolution towards sustainability. The interplay of regulations, market incentives, and technological advancements will determine the pace and scale of hydrogen’s role in the energy transition. As the clean hydrogen economy expands, our approach to measuring and managing its environmental impact must evolve in tandem, ensuring that a greener future is within reach.

For more information about our clean hydrogen services, contact:

There has been a growing focus on Scope 1, 2, and 3 carbon emissions, both in governmental body legislation and individual company climate goals. But what do they really mean? And how does a company search up and down its supply chain to account for its emissions? The carbon experts at EcoEngineers will describe these scopes and how to measure and report them, with an emphasis on Scope 3 demands. Through the lens of a plastic bottle manufacturer, we will discuss the reporting options, potential uses of the data, next steps for companies facing greenhouse gas reporting requirements, and how these measurements can put your company at a competitive advantage above other firms. We hope you can join us!

Summary of the Production of Clean Hydrogen Credits Under Section 45V of the Internal Revenue Code

The U.S. Department of the Treasury (Treasury Department) and the Internal Revenue Service (IRS) on December 22, 2023, released proposed regulations for the Section 45V Credit for the Production of Clean Hydrogen. The proposal contains rules for lifecycle greenhouse gas (GHG) emissions, verification of projects, and modification/retrofitting of clean hydrogen facilities in relation to the tax credit.

Highlights

Lifecycle GHG emissions will be calculated through the point of production (well-to-gate) using the most recent version of the 45VH2—GREET (Greenhouse gases, Regulated Emissions, and Energy use in Technologies) model, considering hydrogen production pathways and feedstocks included in the new 45VH2-GREET model.

Taxpayers can show that electricity used in the hydrogen production process is from a specific source, rather than the grid, by acquiring and retiring Energy Attribute Certificates (EACs) for each unit of energy produced and used. Eligible EACs are to be recorded through a registry/accounting system and meet requirements on incrementality, temporal matching, and delivery.

Third-party verification of the production and sale of the hydrogen is required for each tax year. Verification is also needed for EACs purchased and retired.

Credit for facility modification applies to facilities that did not produce clean hydrogen before January 1, 2023, or were modified to be able to produce under 4 kilograms CO2e per kilogram of hydrogen.

There are no proposed rules relating to renewable natural gas (RNG) used to produce hydrogen, although the final rules may require that for an emissions value to be consistent with the RNG/fugitive methane used, the gas must originate from the first productive use.

A Qualified Clean Hydrogen facility is defined as a single production line used to produce hydrogen to the point of production.

Section 45V credits are available for hydrogen produced in the U.S. or a U.S. territory and sold or used within or outside the U.S.

Comment Period

Comments on the NPRM are due by February 26, 2024. Given the need for additional clarity and guidance from Treasury/IRS on key issues, EcoEngineers is available to assist you with the analysis of the proposed regulations and the preparation of comments. Areas to focus on in written comments include the impact of the proposed regulations on project development plans, including how the proposed regulations may result in revised investment decisions, with associated impacts on domestic manufacturing, jobs, and participation in Regional Clean Hydrogen Hubs.

For more information, please contact Tanya Peacock, Managing Director, Hydrogen, at tpeacock@ecoengineers.us.

Full Summary

Proposed regulations for the Section 45V Credit for Production of Clean Hydrogen were released on December 22, 2023, containing rules for lifecycle GHG emissions, verification of projects, and modification/retrofitting of clean hydrogen facilities in relation to the tax credit. Comments on the proposed rule must be received by February 26, 2024. A proposed hearing is scheduled for March 25, 2024, at 10 a.m. ET. Requests to testify must be received by March 4, 2024.

In addition to the Notice of Proposed Rulemaking (NPRM), the Administration released the new 45VH2-GREET 2023 model and accompanying manual, a letter from the U.S. Environmental Protection Agency (USEPA) that outlines guidance to the Treasury Department regarding reference to the Clean Air Act in 45V, and a U.S. Department of Energy (DOE) whitepaper that supports the approach taken in the proposed regulations to assessing the lifecycle GHG emissions of electricity used to produce hydrogen.

Taxpayers may rely on these proposed regulations for taxable years beginning after December 31, 2022, and before the date the final regulations are published in the Federal Register, provided taxpayers follow the proposed regulations in their entirety and in a consistent manner.

Determination of Lifecycle GHG Emissions

Lifecycle GHG emissions will be calculated through the point of production (well-to-gate) using the most recent version of the 45VH2—GREET model. Factors considered in lifecycle emissions include feedstock growth, gathering, extracting, processing, and delivery to the facility, and emissions in the production process, including electricity used and carbon capture and sequestration (CCS) done by the facility.

The “most recent version” of the 45VH2-GREET model is considered the model that is publicly available on the first day of each taxable year of which the hydrogen claimed under 45Q was produced. If a newer version is available after the first day of the taxable year, it can be used at the taxpayers’ discretion.

Hydrogen Pathways and Feedstocks

Hydrogen production pathways and feedstocks included in the new 45VH2-GREET model include:

Steam methane reforming (SMR) of natural gas, with potential carbon capture and sequestration (CCS)

Autothermal reforming (ATR) of natural gas, with potential CCS

Steam methane reforming (SMR) of landfill gas with potential CCS

ATR of landfill gas with potential CCS

Coal gasification with potential CCS

Biomass gasification with corn stover and logging residue with no significant market value with potential CCS

Low-temperature water electrolysis using electricity

High-temperature water electrolysis using electricity and potential heat from nuclear power plants

Petitions can be filed for a Provisional Emissions Rate (PER) if the GHG emissions rate for feedstock or production technology is not included in the most recent GREET model. An emissions value will have to be requested from the DOE and then included with a PER petition. Following acceptance of the emissions value and PER, the emissions value may be used to calculate credit under 45V. The PER process will only address hydrogen production pathways using biogas and RNG not included in the 45VH2-GREET 2023 model after the final regulations are issued.

Electricity and Energy Attribute Credits (EACs)

Taxpayers may show electricity used in the hydrogen production process as being from a specific source, rather than the grid, by acquiring and retiring EACs for each unit of energy produced and used. Renewable Energy Certificates (RECs) are included as a form of EACs. Eligible EACs are to be recorded through a registry/accounting system and meet requirements on incrementality, temporal matching, and delivery.

To meet the incrementality requirement, the electric generating facility that supplies the electricity that the EAC is based upon must have a commercial operations date (COD) that is no more than 36 months before the hydrogen production facility is placed in service. An alternative test is the requirements may be met if the electricity generating facility has not had an uprate (increase in nameplate capacity) more than 36 months before the hydrogen facility was placed in service and that electricity is part of the uprated production. Other approaches are also being considered such as an avoided retirement approach, a zero or minimal induced grid emissions approach, and a formulaic approach that would allow a fixed percentage of electricity from all existing clean power generators to qualify based on expected curtailment rates. The Treasury Department is seeking comments on these approaches.

The temporal matching requirement may be met by demonstrating that the EAC is generated within the same hour that it is consumed by the hydrogen facility. However, there is to be a transition rule in place, as the ability to track by the hour is currently limited. Until 2028, the transition rule will allow annual matching.

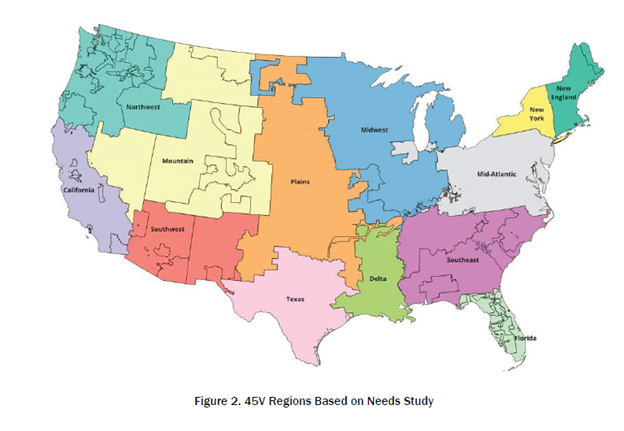

The deliverability requirement is met if the EAC electricity is generated by a source in the same region as the hydrogen facility. “Region” is defined as the U.S. regions defined in the DOE Needs Study. The region hydrogen facilities and generating sources are located is based on the location of the balancing authority to which it is electrically interconnected. The Treasury Department is seeking comments on whether the regions are appropriate as designed, per the table shown below.

Source: DOE

Verification of Production and Sale

Third-party verification of the production and sale of the hydrogen is required for each tax year. Verification is also needed for EACs purchased and retired.

A verification report is to include product attestation, sale or use attestation, conflict attestation, a qualifier verifier statement, general information about the facility (location, production description/method, feedstock, amount of feedstock used, list of metering devices and statement on quality control/calibration/activation), and documentation to substantiate the verification process.

A ”qualified verifier” is an individual or organization with active accreditation as a validation and verification body from the American National Standards Institute (ANSI) National Accreditation Board (ANAB), or a verifier, lead verifier, or verification body under California’s Low-Carbon Fuel Standard (LCFS) program. EcoEngineers has been granted accreditation from ANAB, in accordance with the International Organization for Standardization (ISO) standards ISO/IEC 17029:2019 Conformity assessment — General principles and requirements for validation and verification bodies.

Modification of an Existing Facility

Credit for facility modification applies to facilities that did not produce clean hydrogen before January 1, 2023, or were modified to be able to produce under 4 kilograms CO2e per kilogram of hydrogen. The date placed into service for modified facilities will be changed to the date the property required to complete the modification is placed in service. Existing facilities may have the date placed into service updated to the date that new property is added, so long as the used property is not more than 20% of the facility’s total value (80/20 rule). Replacing natural gas with biogas or renewable natural gas in the hydrogen production process does not qualify as a facility modification under the proposed rules.

RNG and Fugitive Sources of Methane

There are no proposed rules relating to RNG used to produce hydrogen, though it is suggested that the final rules may require that for an emissions value to be consistent with the RNG/fugitive methane used, the gas must originate from the first productive use. Otherwise, the gas would be given an emissions value consistent with natural gas. Attribute certificates would need to be acquired and retired to demonstrate procurement of the gas and that environmental attributes are not being sold to other parties or used for compliance with other policies and programs. Additionally, hydrogen producers would be required to have a pipeline interconnection and measurement using a revenue grade meter. There are 12 questions listed in the proposed rules asking for comments relating to RNG/fugitive methane used in hydrogen production.

Additional Rules

A Qualified Clean Hydrogen facility is defined as a single production line used to produce hydrogen to the point of production. A single production line is defined as all components of property that function interdependently to produce hydrogen. Electricity production equipment is not included in the definition of a facility. Components with purpose in addition to the production of hydrogen may be part of the facility if they function interdependently with other components to produce the hydrogen.

The “taxpayer” is who owns the hydrogen facility at the time of production to which the credit is claimed, regardless of if they are the “producer.” Credit is determined for all produced in a hydrogen taxable year, regardless of whether verification or sale of produced hydrogen occurred in that year. Still, the credit cannot be claimed until verification occurs. Thus, the taxpayer would have to file an amended return or administrative adjustment if verification occurs after the return filing deadline.

An anti-abuse rule is to be implemented to make credit unavailable if the purpose is to produce in a wasteful way. This includes if the taxpayer knows, or has reason to know, that the hydrogen produced is to be vented, flared, or used to create additional hydrogen.

Section 45V credits are available for hydrogen produced in the U.S. or a U.S. territory and sold or used within or outside the U.S.

Tanya Peacock

For more information, please contact Tanya Peacock, Managing Director, Hydrogen, at tpeacock@ecoengineers.us.

U.S. Treasury and IRS Release Guidance on Section 40B Sustainable Aviation Fuel (SAF) Credits

On December 15, 2023, the U.S. Treasury Department and the Internal Revenue Service (IRS) provided initial guidance regarding sustainable aviation fuel (SAF) tax credits under Section 40B of the Internal Revenue Code, enacted by the Inflation Reduction Act of 2022 (IRA). The following information contains highlights of this notice. Producers will find guidance in relation to SAF credits, lifecycle analysis, verification requirements, and an emissions-reduction safe harbor.

Specifically:

The Renewable Fuel Standard (RFS) methodology for calculating lifecycle emissions may be used to determine emission reductions for SAF credits and new Greenhouse Gases, Regulated Emissions, and Energy Use in Transportation (GREET) models to determine emission reductions for the credit to be released early in 2024.

SAF synthetic blending components must be Quality Assurance Program (QAP)-validated.

Synthetic blending components have been assigned an emission-reduction percentage of 50%-60%, depending on the D-Code it is produced under.

Full Summary

Section 13203 of Public Law 117-169, 136 Stat. 1818 (August 16, 2022), commonly referred to as the Inflation Reduction Act of 2022, added §§ 40b with amendments to §§ 38(b), 40A, 87, 4101(a), 6426, and 6427(e)(1), to establish credits for fuel mixtures containing Sustainable Aviation Fuel (SAF). The SAF credit is equal to 1) the number of gallons of SAF in a qualified mixture, multiplied by the sum of 2) $1.25 and 3) the “applicable supplementary amount.” The applicable supplementary amount is $0.01 for each percentage point the emissions reduction percentage of the SAF exceeds 50%. The maximum applicable supplementary amount is $0.50 per gallon.

Credit may be issued for SAF with emissions reductions of at least 50% as compared to petroleum-based jet fuel. Emissions reductions, as listed in the code, are defined by the most recent Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), or similar methodology that satisfies § 211(o)(1)(H) of the Clean Air Act. Prior guidance of the rule has been released in Notice 2023-6 pertaining to credit and payment rules, as well as CORSIA-based safe harbors for emission-reduction percentage determination. The notice did not, however, provide guidance for calculating the emission-reduction percentage or the certification requirements. Notice 2024-6 sought to do so by allowing the methodology of the U.S. Renewable Fuel Standard (RFS) program to be employed for greenhouse gas (GHG) emissions calculations and providing guidance in relation to third-party validation.

Notice 2024-6 states the methodology employed by the RFS program for determining lifecycle GHG emissions is designed to satisfy § 211(o)(1)(H) of the Clean Air Act, and thus, is similar to and can be used for calculating the GHG emissions percentage reductions for the SAF credit. Existing GREET models have been determined insufficient to be used to calculate lifecycle GHG emissions for the purpose of this credit. The U.S. Department of Energy (DOE) is in the process of creating an updated GREET model which, subject to release and further guidance, is anticipated to satisfy the requirements of 40b(e)(2) and be used for the calculation of emission-reduction percentages for SAF sold and used after December 31, 2022, and before January 1, 2025. The release of the updated GREET model is expected in early 2024.

The U.S. Internal Revenue Service (IRS) will accept the emission-reduction percentage of SAF of a synthetic blending component that qualifies as a renewable fuel in the RFS program and is produced under ASTM International (ASTM) D7566. The synthetic blending component must be Quality Assurance Program (QAP)-validated. Producers of the SAF synthetic blending component must record the valid Q-RINs (Renewable Identification Numbers) on the Certificate for SAF Blending Component included in Appendix A of Notice 2024-6. This certificate supersedes the model certificate included in Appendix B of Notice 2023- 6. In addition to QAP validation, producers/importers must also show third-party certification demonstrating compliance with general requirements, supply chain traceability requirements, and information transmission requirements concerning the Life-Cycle Analysis (LCA).

Synthetic blending components produced under D-Codes 4 and 5 will be assigned an emissions-reduction percentage of 50%, and fuel produced under D-Codes 3 and 7 will be assigned a 60% emissions-reduction percentage. The IRS will accept emissions reduction percentages for facility-specific pathways for producers of jet fuel under D-Codes 3, 4, 5, and 7, so long as the fuel is QAP-verified. Specific LCA point estimates published by the U.S. Environmental Protection Agency (USEPA) beyond the 50%-60% safe harbor will not be accepted by the IRS.

The following crediting example was provided:

A blender used 100,000 gallons of a SAF synthetic blending component to produce a SAF-qualified mixture. The SAF synthetic blending component has generated cellulosic diesel (D-code 7) RINs under a pathway that qualifies under the RFS program, and these RINs were validated under a QAP. The final rule that added the pathway to the list of approved renewable fuel production pathways in the RFS regulations states that the jet fuel’s emissions reduction percentage compared to the baseline is 64%. However, for purposes of calculating the applicable supplementary amount, the emissions reduction percentage will be deemed to be 60% under the safe harbor described in section 3.01(2) of this notice, which corresponds to the emissions reduction threshold the fuel was required to meet to qualify as cellulosic diesel and thus generate D-code 7 RINs. The per-gallon amount of the SAF credit with respect to the SAF-qualified mixture described above is calculated by adding $1.25 and the applicable supplementary amount, if any, with respect to the SAF synthetic blending component used to produce the SAF-qualified mixture. Here, the SAF synthetic blending component qualifies for the applicable supplementary amount, because the emissions reduction percentage is deemed to be 60%. The applicable supplementary amount is calculated by subtracting 50 from the emissions reduction percentage (60), and then multiplying by the applicable rate ($0.01): (60 – 50) × $0.01 = $0.10 per gallon. The total amount of the SAF credit is calculated as follows: 100,000 gallons × ($1.25 + $0.10) = $135,000.00.

The long-awaited and much-anticipated draft rulemaking for California’s Low-Carbon Fuel Standard (LCFS) is out. Some significant changes, even from the Standardized Regulatory Impact Assessment (SRIA), were outlined in September.

Below are some initial highlights/summary points from the 146-page release:

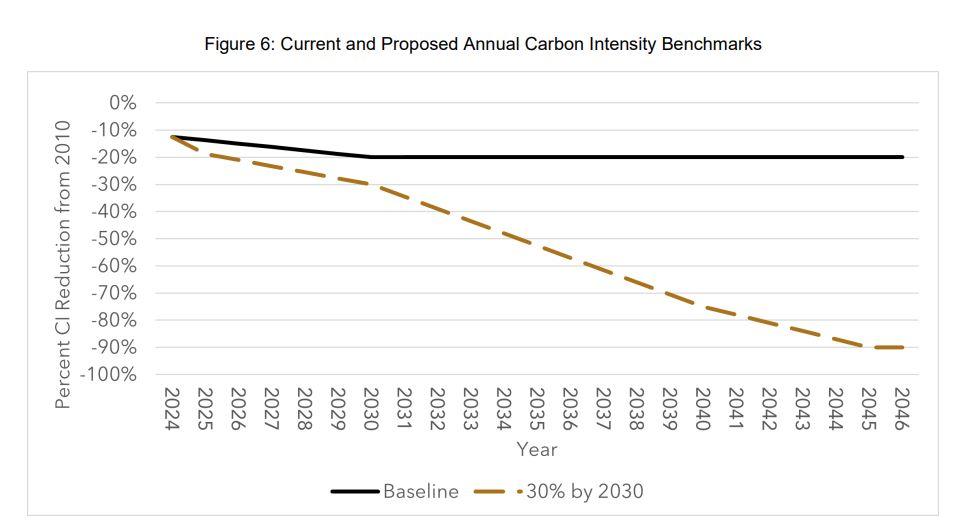

California’s Air Resources Board (CARB) is increasing the 2030 compliance target from 20% to 30% and 90% by 2045. This probably isn’t enough to immediately impact LCFS credit prices in the short term. Our modeling and analysis show potential increasing LCFS credit prices in the latter parts of the decade (even with the auto-acceleration mechanism, AAM).

Dairy/swine projects that rely on avoided methane emission crediting and breaking ground after December 31, 2029, will be subject to credit phase-out. Crediting will be available through 2040 for compressed natural gas (CNG) usage and through 2045 for renewable natural gas (RNG) used to produce hydrogen. Facilities that break ground before the end of 2029 will be able to generate credits for 30 years following approval of the application.

The RNG deliverability/book and claim issue that concerned many people in the SRIA will happen, but CARB greatly extended the timelines. Deliverability requirements will follow the RNG/CNG pathway phase out and projects that break ground after 2029 will be required to demonstrate physical deliverability requirements beginning in January of 2041. Biomethane used as an input for hydrogen production will have deliverability requirements starting January 1, 2046. Projects that break ground before 2030 are not subject to deliverability requirements. Deliverability requirements apply to biomethane fuel pathways only and would not apply to biomethane used in hydrogen fuel pathways.

Sustainable aviation fuel (SAF) used in intrastate air travel will not be exempt from the LCFS program beginning in 2028.

Several changes to simplify the Tier 1 calculators and add a Tier 1 hydrogen calculator. Updates to the Tier 1 calculator are to include updated emissions factors, streamlined inputs, and a new layout. Temporary Pathways and Lookup Table carbon intensity (CI) values are to be updated for specified pathways.

The energy economy ratio (EER) for electric forklifts is reduced by 50% for forklifts less than 12,000 pounds. This will cut the credits generated in half. In addition, direct metering of electricity used in electric forklifts will be required.

Zero-emission vehicle (ZEV) infrastructure crediting is being expanded to include medium-and-heavy duty infrastructure and extend light-duty infrastructure crediting. Additional changes are to occur for non-metered residential electric vehicle (EV) charging as well, two of which include changing the scope of the Clean Fuel Reward to a medium-and-heavy duty rebate and expanding the proportion of credit proceeds required to be invested in disadvantaged, low-income, rural, and tribal communities.

Credits from petroleum projects are to be phased out by 2040, but carbon capture and sequestration (CCS) projects are to be excluded from the phase-out proposal.

Direct air capture (DAC) with sequestration project credits will be limited only to projects located in the U.S. This will not apply to DAC-to-fuel projects submitted as Tier 2 Alternative Fuel Pathways.

New requirements are to be put in place to track the supply chain of crop-based and forestry-based feedstocks to their point of origin and require independent feedstock certification. In addition, palm-derived fuels will no longer be eligible for generation.

Book-and-claim allowance is being expanded to include low-CI hydrogen injected into the pipeline network physically connected to California. The well-to-wheel CI threshold for low-carbon hydrogen is to be less than or equal to 55 g/MJ (grams per megajoule) for gaseous hydrogen and 95g/MJ for liquid hydrogen. Hydrogen from fossil gas will be excluded from book-and-claim, with some exceptions. Additionally, power purchase agreements for low-CI electricity will allow for hydrogen used as a transportation fuel.

CARB is proposing to add new verification requirements on electric technologies, some of which include EV-charging transaction types, fuel cell vehicle fueling transaction types, and fixed guideway electricity fueling.

Bottom line – get your RNG projects developed before 2030 to be eligible for up to 30 years of crediting. Crop-based/forestry-based feedstock fuels will have significant traceability and certification requirements. Several rules on hydrogen production, dispensing, and crediting are to be put in place. Multiple technologies and fuel pathways will be seeing changes in credit eligibility and new requirements.

CARB gets a lot of flak but, after an initial read, they seem to have done a good job balancing all interests along with providing more clarity across many issues. This proposed rulemaking greatly strengthens the LCFS program through 2045.

There is a lot more in the draft and our team is reviewing it in more detail. Stay tuned for a deeper analysis.

In late June, the U.S. Environmental Protection Agency (USEPA) released the long-awaited Set Rule final language for its Renewable Fuel Standard (RFS). Although the pathway for the generation of Renewable Identification Number (RIN) credits associated with renewable electricity and vehicle charging (eRINs) was removed, other highly significant changes impacting the biogas and renewable natural gas (RNG) industry were retained. One of those important changes includes RIN apportionment between D3 and D5 RINs whereby digesters can now continue to generate D3 RINs through biogas or RNG from wastewater or manure, and further generate D5 RINs through any additional biogas or RNG produced from accepting and co-digesting food waste. This effectively allows digesters to capture D3 RIN revenue that was not previously possible.

Learn more from the technical and regulatory experts at EcoEngineers on how your biogas and RNG projects can benefit from this newly implemented change.

This webinar originally aired on December 6, 2023.

The Inflation Reduction Act (IRA) signed into law August 2022 contains potentially more than $100 billion of tax incentives over its lifetime. Project developers have the opportunity to seize on and set in motion a rapid-growth pathway for the clean hydrogen economy. This 10-year tax credit is extremely valuable and represents a substantial share of the economic proposition for clean hydrogen production. Specifically, the IRA’s 45V tax credit requires emissions from hydrogen production to meet a low-carbon threshold on a well-to-gate life-cycle basis. To determine eligibility, project developers need a carbon intensity (CI) score.

In this webinar, EcoEngineers will speak about carbon Life-Cycle Analysis (LCA), including factors that affect CI, project eligibility and compliance, and delve into strategies for project developers to navigate regulatory uncertainty effectively and share practical guidance on technology selection.

This webinar originally aired on November 16, 2023.

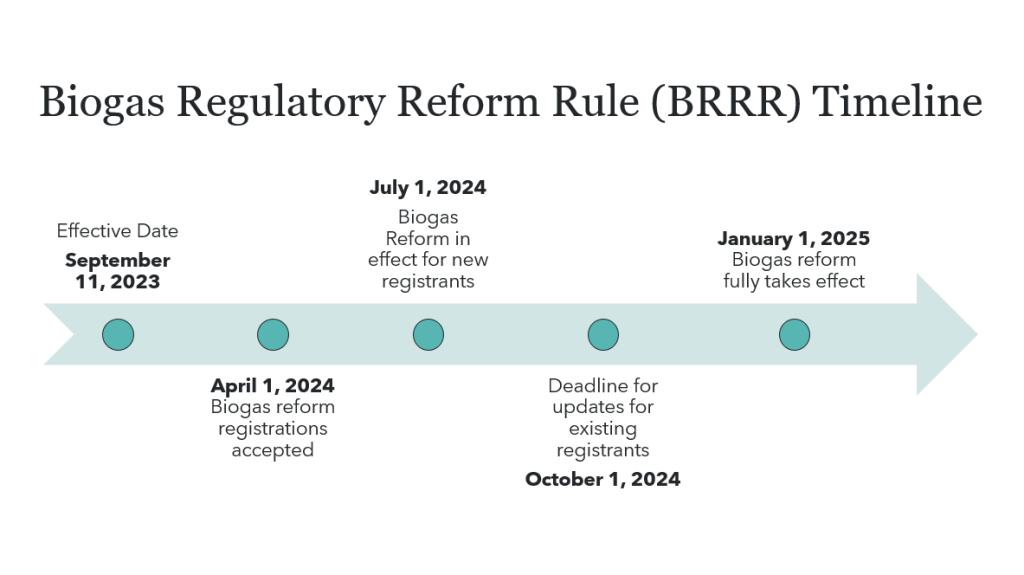

Understanding the implementation of the Biogas Regulatory Reform Rule (BRRR) within the finalized Renewable Fuel Standard (RFS) Set Rule released in July continues to be the talk of the industry. With the significant changes, many entities are trying to understand the U.S. Environmental Protection Agency’s (USEPA) intent, seeking USEPA clarification, and trying to understand how these new rules impact their planned, in-construction, and operational renewable natural gas (RNG) assets. As the USEPA develops its guidance, we understand that the industry needs time to prepare for the new regulatory requirements effective on July 1, 2024, for new facilities, and January 1, 2025, for existing pathways.

With that in mind, Eco is taking a multi-phased approach to BRRR implementation, including:

Monthly meetings with the USEPA.

In-person meeting with the USEPA held in late October.

Internal working group that meets weekly.

Proposed regular in-person meetings with the USEPA.

Participation in RFS Set Rule and biogas reform discussions and committees in industry trade associations.

We understand the urgency needed to address outstanding questions and we will continue to work with the USEPA to get the clarity necessary to comply with the new rules.

Proactively Addressing the Outstanding Questions and Issues

Eco is drafting its implementation plan for the RFS Set Rule and the BRRR. We will present our proposal to the USEPA for approval in the following areas:

Proposed approach to the RFS registration process changes and how to meet the requirements, consistent with the USEPA’s intent of the RFS Set Rule.

Proposed schedule and process to get our Quality Assurance Program (QAP) protocols updated to meet the new RFS Set Rule, which will provide more compliance clarity to our QAP customers.

We expect to have these proposed process changes sent to the USEPA within the next few weeks and will encourage the USEPA to sign off on our approach so we can move to the implementation phase, and have a definitive process for addressing metering/monitoring, RFS registration, and QAP questions and issues.

Eco is also working with equipment vendors to understand whether their equipment meets the formalities of the RFS Set Rule with the goal of producing a list of equipment and vendors that meet the regulation requirements.

Eco will provide monthly updates or webinars to update the industry on the progress made, learnings, timelines, and remaining issues/questions.

Eco is already working with several clients and can help you with:

Understanding the regulation changes and how they impact planned or operational renewable natural gas (RNG) facilities.

Metering and measurement reviews.

RFS registration amendments and third-party engineering reviews for existing facilities.

Compliance assistance.

D3/D5 Renewable Identification Number (RIN) split analysis and methodologies.

Our team is ready to assist you with working through your questions and issues to successfully comply with the new regulations. If you haven’t already, the time to start is now and Eco can be your guide through this transition period. Please reach out to us with any questions or issues.

For more information about the implementation of the BRRR and/or the RFS Set Rule, please contact:

With several state, federal, and voluntary carbon market (VCM) incentives available, the ethanol industry has a unique opportunity to reinvent itself. The range of clean fuel regulations across the U.S. and Canada, along with the IRA and bipartisan Infrastructure Law, provide new opportunities to decarbonize ethanol.

In this webinar, we discuss how ethanol producers can incorporate technologies such as carbon capture and sequestration (CCS), hydrogen, renewable natural gas (RNG), biomass based heat, renewable electricity, and sustainable agriculture to significantly lower the carbon intensity (CI) of their products in order to access future compliance, voluntary and sustainable aviation fuel (SAF) markets.

In addition, we will discuss why partnerships with supply chains that embrace sustainable farming practices create a holistic approach to reducing the CI score of an ethanol plant’s products and overall carbon footprint. Our expert panelists will dissect the potential benefits, challenges, the regulatory landscape shaping this transformative journey, and provide recommendations on how ethanol producers can successfully chart a path toward a greener, more sustainable future.

This webinar originally aired on October 24, 2023.

The U.S. Department of Energy’s H2Hubs Program: Accelerating the Clean Hydrogen Economy

By Tanya Peacock

In a world increasingly focused on sustainable and eco-friendly solutions, clean[1] hydrogen has emerged as a promising alternative for a low-carbon energy future. On October 13, 2023, the Biden-Harris Administration announced seven U.S. regional clean hydrogen hubs spanning 16 states: Appalachian, California, Midwest, Gulf Coast, Heartland, Mid-Atlantic, and Pacific Northwest. Hubs are set to receive $7 billion in Bipartisan Infrastructure Law (BIL) funding under the U.S. Department of Energy’s (DOE) Regional Clean Hydrogen Hubs Program (H2Hubs). An additional $1 billion will be used for demand-side support to encourage industrial decarbonization and other innovative end uses. Together with an expected $42 billion in private investment, the Hubs Program represents a $50 billion investment in clean hydrogen.

The seven H2Hubs are the beginning of a national network of clean hydrogen producers and consumers, together with hydrogen storage and transportation, while supporting hundreds of thousands of new construction and permanent jobs. Skill sets required to support the clean hydrogen economy are similar to many oil and gas jobs. This is important as the energy transition accelerates so that workers in traditional energy sectors aren’t left behind.

In looking at the map below, there are areas of the country without H2Hub projects, noticeably the southwestern, northeastern, and southeastern regions, and Hawaii. The momentum created by the application and selection process is an important start and hopefully will continue to build and expand beyond the selected applications. To achieve a clean hydrogen economy, we need a nationwide network of hydrogen producers, consumers, and connective infrastructure. For example, to decarbonize long-haul, heavy-duty trucking, we will need transportation corridors with a network of H2 fueling stations. To accomplish this, ideally, selected H2Hubs will begin collaborating early-on with nearby regions that weren’t selected to leverage ideas, expertise, and resources, to accommodate the 8-10 year phased contracting approach.[2]

[1] Clean hydrogen is defined by the U.S. Department of Energy (DOE) as hydrogen produced with a carbon intensity equal to or less than 4 kilograms of CO2e produced on a well-to-gate basis per kilogram of hydrogen produced. (https://www.hydrogen.energy.gov/library/policies-acts/clean-hydrogen-production-standard)

[2] The phased contracting process, as described by OCED, is divided into 4 parts post-selection, and will take between 8-10 years: Phase 1 is the detailed planning process and is ~ 12-18 months; Phase 2 is project development, ~2-3 years; Phase 3 is construction, ~ 3-4 years; and Phase 4 is ramp-up and operations, ~ 2-4 years.

Source: Office of Clean Energy Demonstrations website

The H2Hubs are expected to collectively produce three million metric tons of hydrogen annually, reaching nearly a third of the 2030 U.S. production target and lowering emissions from hard-to-decarbonize industrial sectors that represent 30% of total U.S. carbon emissions, according to a statement issued by the DOE. Together, they will also reduce 25 million metric tons of carbon dioxide (CO2) emissions from end-uses each year—an amount roughly equivalent to the combined annual emissions of 5.5 million gasoline-powered cars. These are the figures from the press releases. To build confidence in the use of hydrogen for decarbonization, more transparency around how the projects’ community and environmental benefits are calculated will be required as the negotiation process between DOE and the selected applicants progresses and contractual agreements are finalized.

Of the 7 selected Hubs, targeted end uses include sectors that today use hydrogen from natural gas without carbon capture such as refineries, petrochemicals, and fertilizer production, and newer uses such as port operations, marine fuel, trucking, ammonia, space heating, and power generation. Clean hydrogen (production, processing, delivery, storage, and end-use) is crucial to the DOE’s strategy for achieving President Biden’s goal of a 100% clean electrical grid by 2035 and net-zero carbon emissions by 2050 because of the huge decarbonization potential.

The success of the H2Hubs and development of the clean hydrogen industry more broadly is directly linked to the Inflation Reduction Act (IRA) 45V hydrogen production tax credit (PTC). Hydrogen stakeholders have been waiting for the issuance of the IRA 45V PTC guidance document by the Internal Revenue Service (IRS) for more than a year since the IRA was signed into law. Key questions contributing to the delay center around how to increase certainty that the production and use of clean hydrogen will have a net environmental benefit and allow the flexibility needed to allow a nascent industry to develop and scale up.

Long-term techno-economic decarbonization models show that even with massive electrification and energy efficiency improvements, in 2050 as much as 50% of final energy demand globally will be met with clean molecules. The H2Hubs will play an important role demonstrating how clean hydrogen can scale up and in what sectors of the economy it can have the biggest decarbonization impact.

EcoEngineers Can Help Guide Your Clean Hydrogen Project

As companies seek to navigate the emerging clean hydrogen landscape, EcoEngineers can help project developers and their stakeholders address the factors that impact carbon intensity (CI) for clean hydrogen projects. Specifically, here’s how EcoEngineers can help:

Life-Cycle Analysis (LCA): Eco can provide comprehensive LCA services that assess the environmental impacts of clean hydrogen production, from raw material extraction to end use. Having performed more than 500 LCAs since 2015, we have experience in all regulations that require LCAs, including the U.S. Renewable Fuel Standard (RFS), California Low-Carbon Fuel Standard (LCFS), Oregon Clean Fuels Program (CFP), Canada Clean Fuel Regulations (CFR), British Columbia Renewable and Low-Carbon Fuel Requirements (RLCFR), Brazil RenovaBio, EU Renewable Energy Directive (RED) and impending directives, along with emerging Voluntary Carbon Markets.

Carbon Intensity (CI): We can help businesses lower their CI by identifying opportunities for efficiency improvements and carbon reduction strategies in clean hydrogen production and utilization. Lower CI values are crucial for meeting sustainability goals and accessing available incentives and credits such as the 45V clean hydrogen production tax credit under the Inflation Reduction Act (IRA).

Project Eligibility and Compliance: Navigating the regulatory landscape is complex, and EcoEngineers can guide businesses through the process. We can ensure that projects meet eligibility requirements for incentives, grants, and compliance with federal and state regulations. With more than 200 asset development engagements and $4 billion of investments for projects across decarbonization projects and technologies, Eco’s team of experts can provide individualized guidance throughout the entire project development lifecycle of your hydrogen project. From design, build, and operational phases to regulatory and permitting guidance, technology and market risk assessments, startup optimization, and capital raising evaluations – we have you covered.

Technology Selection: We can also provide practical guidance on technology selection, helping businesses choose the most suitable and efficient technologies for clean hydrogen production and utilization.

About EcoEngineers

EcoEngineers is a consulting, auditing, and advisory firm with an exclusive focus on the energy transition. From innovation to impact, Eco helps its clients navigate the disruption caused by carbon emissions and climate change. Eco helps organizations stay informed, measure emissions, make investment decisions, maintain compliance, and manage data through the lens of carbon accounting. Its team of engineers, scientists, auditors, consultants, and researchers live and work at the intersection of low-carbon fuel policy, innovative technologies, and the carbon marketplace. Eco was established in 2009 to steer low-carbon fuel producers through the complexities of emerging energy regulations in the United States. Today, Eco’s global team is shaping the response to climate change by advising businesses across the energy transition.

Tanya Peacock

For more information about our clean hydrogen services, contact: